Continued Low Interest Rate Environment – Regulatory Help Could Be on the Way

Entering the twelfth year of historically low interest rates, and with the Federal Reserve indicating rates will stay low for at least the next two years, banks are having a harder time than ever finding yield. With net interest margins falling to a record low, BOLI has become an even more popular alternative investment for banks searching for returns. Particularly in 2020, with a pandemic taking its toll on the economy and the 10-year treasury hovering just over 100 basis points in early 2021, banks are seeking yield and have found it in BOLI. In the third quarter of 2020 alone, there were approximately 97 purchases of $1,000,000 or more of BOLI totaling over $1 billion in premium. Contributing to the growth of the marketplace, 9 of those purchases were made by first time BOLI buyers.

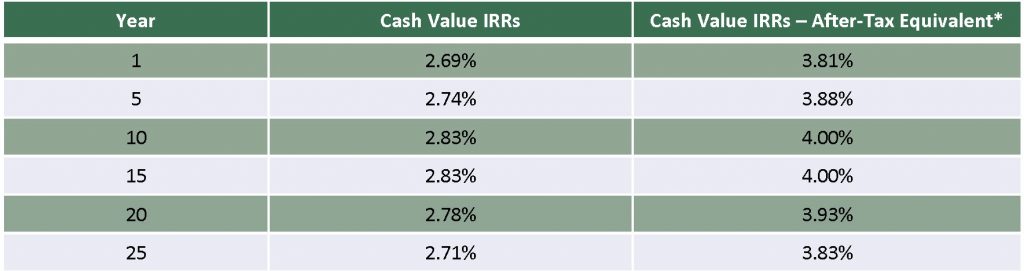

Attractive returns combined with tax free growth offered in BOLI policies are behind the large volume of cases. The table below illustrates expected returns from a BOLI policy purchased on a 45-year-old male.

*Assumes 29% Corporate Tax rate

Regulatory Relief

The very last session of congress in 2020 generated a somewhat surprising but beneficial result for the life insurance consumer. Life insurance products are governed by IRC Section 7702, which imposes several requirements on every policy sold. In many cases, 7702 forced banks to buy a specific form of life insurance called a modified endowment contract (MEC) to generate the rate of return they were seeking. MECs still provide banks with favorable tax treatment and returns but limit the liquidity that could be generated from the policies – a hurdle too high to overcome for some banks.

However, changes made by the Consolidated Appropriations Act will allow most life insurance products to be more efficient and generate higher rates of return relative to past products. The new 7702 could have profound impacts on how banks buy life insurance by allowing them to buy policies with the higher rates of return they seek without the liquidity issues they ran into in the past. Beneficial impacts brought on by changes to Section 7702 combined with higher corporate tax rates signaled by the new administration will make BOLI a premier asset for banks in 2021.

If you have questions about BOLI or would like to explore an investment, please contact your Mullin Barens Sanford consultant.

About Mullin Barens Sanford Financial

Through a powerful combination of independence and experience, Mullin Barens Sanford Financial and Insurance Services (MBS Financial) is a leading consulting firm that assists companies with 409A and other executive benefit needs.

Disclaimer: The materials are designed to convey accurate and authoritative information concerning the subject matter covered. However, they are provided with the understanding that Mullin Barens Sanford does not engage in the practice of law, or give tax, legal or accounting advice. For advice in these areas please consult your appropriate advisors.

© 2025 Mullin Barens Sanford Financial and Insurance Services, LLC. All Rights Reserved.

1421 Emerson Avenue, Oxnard, California 93033 | Website: www.mbsfin.com

Securities offered through M Holdings Securities, Inc., a Registered Broker/Dealer, Member FINRA/SIPC. #4444620