No, DCPs restore lost savings opportunities and fit in an egalitarian culture.

Many companies say yes. Here are the reasons why:

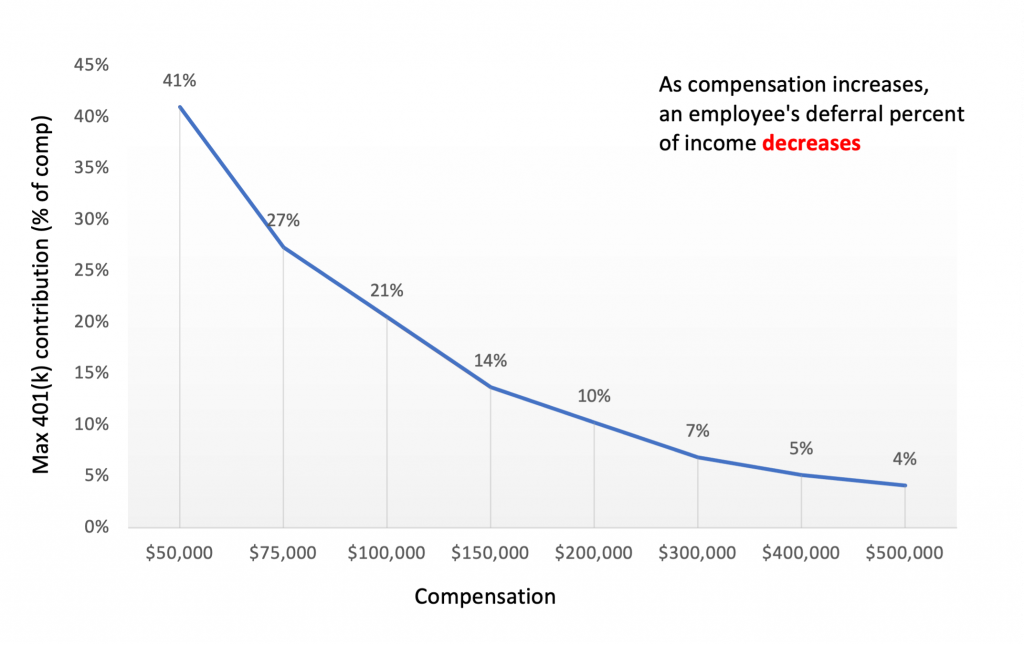

Issue: Highly compensated employees (HCEs) are in fact discriminated against by 401(k) contribution limits and testing. In 2022, an HCE is defined by the IRS as having total compensation of $135k or more (IRC Section 415).

Unfair 401(k): An employee under age 50 earning $200k in 2022 can only defer a maximum of 10.25% ($20,500) in the 401(k). The same employee earning $100k could defer 20.5% of their income ($20,500). This difference compounds yearly and negatively affects the replacement income ratio of the HCE approaching retirement.

Why 401(k)s Are Not Enough for HCEs

How can the plan sponsor make up for the reduced deferral opportunity that can affect HCEs in the 401(k)?

Potential Solution: The employees affected by 401(k) limits can be offered a nonqualified Deferral Restoration Plan (DCP). To keep the plan egalitarian, it is possible to design the plan to only allow the affected employees the ability to defer the same percentage of the same income that the 401(k) allows.

Proxy Disclosure: Companies that strive to be egalitarian may also be concerned about the optics of offering a Deferral Restoration Plan. Here are some examples of proxy disclosures for companies that have a 401(k) Deferral Restoration Plan:

- No pension or other special benefits

- No significant perquisites

- We do not provide excessive perquisites, benefits or severance benefits

- No excessive perks

- No excessive pension or SERPs

Conclusion: Deferral plans are flexible and can be customized to meet the specific needs of the plan sponsor. They are an important element of tax planning for key employees and can be a valuable tool for managing several types of taxable income including restricted stock units (RSUs). These tax management benefits can assist companies in efforts to recruit and retain the best employees. Over 90% of large companies (over $1B revenue) already offer at least one deferral plan(1). If your company strives to maintain egalitarian benefits, then it should consider restoring its HCEs’ ability to defer income for retirement at the same rate as its non-HCEs.

For more information about how to design a deferral plan that helps the company provide equal deferral opportunities to its HCEs, please contact your Mullin Barens Sanford Consultant via this link.

(1) Compensation, Retirement and Benefits Trends Report, Newport Group, 2018/2019

Disclaimer: The materials are designed to convey accurate and authoritative information concerning the subject matter covered. However, they are provided with the understanding that Mullin Barens Sanford does not engage in the practice of law, or give tax, legal or accounting advice. For advice in these areas please consult your appropriate advisors.

© 2025 Mullin Barens Sanford Financial and Insurance Services, LLC. All Rights Reserved.

1421 Emerson Avenue, Oxnard, California 93033 | Website: www.mbsfin.com

Securities offered through M Holdings Securities, Inc., a Registered Broker/Dealer, Member FINRA/SIPC. #4444620