According to statutory filings, US insurance companies own more than $30B dollars of institutional life insurance. This Article describes the basic attributes of ICOLI, the applicable tax and regulatory structure, the available investments, the process to acquire ICOLI and how insurance companies deploy this strategy to increase investment yields.

Insurance companies purchase institutionally priced life insurance to:

- offset or recover employee benefit costs,

- hedge against potential economic loss stemming from the death of an executive,

- provide death benefit coverage based to their management-employees perquisites and

- improve overall investment yield.

ICOLI contracts provide both death benefits when an insured passes away and yield to a cash value account during the life of the insured. The cash value account yields depend on the investment options offered in the contract and selected by the policyowner. This cash value account accumulates and is accounted for as an asset while the insured is living. When an insured passes away, the cash value is paid to the policyowner as part of the contract’s tax-free death proceeds.

How can ICOLI maximize yield

ICOLI maximizes investment yield through tax deferred growth of cash value, tax free death benefits and lower risk-based capital charges than investments held outside of ICOLI. A lower risk-based capital charge allows less total capital to be deployed for a given investment, therefore creating a more efficient deployment of capital.

What investments are available within ICOLI

Investments available within ICOLI contracts are extremely diverse and span multiple asset classes. Commonly included in the offering are fixed income options, various categories and durations of bond funds, growth blend and value equity funds, along with international options, specialty funds and alternative fund strategies.

Companies issuing ICOLI conduct due diligence on the funds and the fund managers they offer within their ICOLI products. Due diligence is conducted both when a fund is proposed to be added to the platform and periodically thereafter to ensure the fund meets the Company standards. Funds that do not meet an issuing company’s qualitative and quantitative standards are not offered or are removed from the platform.

The vast array of investments available within ICOLI make it easy for a purchasing insurance company to match its investment strategy. As investment strategy changes over time, the ICOLI investment allocation can be easily changed in a tax efficient manner. Unlike traditional investments, reallocations within ICOLI are not taxable.

Tax Characteristics

Cash value

Tax-deferred growth is permitted by Internal Revenue Code (“Code”) sections 7702(g) and 72(e), which provide that inside build-up or “gain” is not taxable if the contract continues to meet the definition of life insurance under Code section 7702(g) and no taxable distributions are made from the policy under Code section 72(e). The same code sections apply to tax-free reallocations within ICOLI.

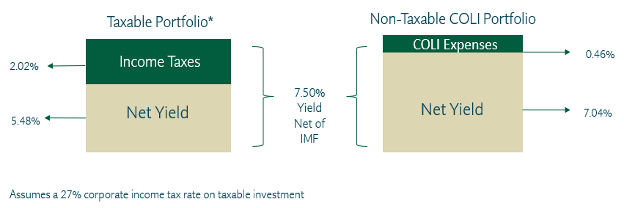

Cost of insurance charges are typically less than income taxes, resulting in an increased yield over a taxable portfolio.

Death Benefit

ICOLI contracts provide tax-free death proceeds when the contract’s insured passes away. For a company to receive this tax free death benefits, code section 101(j) requires the policyowner at the time of purchase to obtain consent from its insureds, and the insureds must be among the top 35% most highly compensated employees of the purchasing insurance company. The company issuing ICOLI provides the purchaser a 101(j) compliant consent form.

Risk-based capital reserving

In addition to tax benefits, ICOLI receives lower potential risk-based capital reserving requirements than investments held outside of ICOLI. The National Association of Insurance Commissioners (“NAIC”) risk-based capital reserving system dictates the amount of capital an insurance company must set aside for various investment risks. Categories of risks covered by risk-based capital reserving are asset risk, insurance risk, interest rate risk and business risk.

The amount of capital required for a given investment depends on the risk factors of the investment. An insurance company purchasing equities may have to set aside a hedge of 30% of the value of the purchased equity to meet this risk-based capital reserve requirement. Yet, if the insurance company purchased ICOLI and allocated to similar equities within the ICOLI contract, the risk-based capital charge would be dramatically less – 0% or 5%.

The risk-based capital charge for all investments made within ICOLI is set at a static rate of 5% for property and casualty insurance companies and 0% for life and health insurance companies. Therefore, an investment in equities within an ICOLI contract will require less capital than an investment in a similar category outside of an ICOLI contract.

In addition to NAIC reserving requirements, ratings agencies have adopted a risk-based capital reserving formula to help grade an insurance company’s financial strength which includes ICOLI investments. For example, AM Best assigns an 0.08 charge to reserves for ICOLI, thus not looking through ICOLI to the underlying investments.

Accounting

Both the Generally Accepted Accounting Principles (GAAP) and the Statements of Statutory Accounting Principles (SSAP) provide clear guidance for ICOLI.

GAAP

Accounting guidance for ICOLI is found in the Accounting Codification Standard 325-30. The cash surrender value of a life policy is entered on the contract owner’s balance sheet as an “Other Asset” and the change in the cash surrender value is entered on the owner’s income statement as “Other Income.”

Sample journal entries

| Premium Payment

Investment in ICOLI Cash |

Debit

$25,000,000

|

Credit

$25,000,000 |

| Change in surrender value

Investment in ICOLI Gain on Investment in ICOLI |

$1,750,000 |

$1,750,000 |

SSAP

SSAP 21(6) provides that the cash surrender value of a life policy is entered on the owner’s statutory balance sheet as “Aggregate Write-ins Other than Invested Assets” on Line 25, with an explanation of the asset in “Details of Write-ins” identified as “Cash Surrender Value of Life Insurance.” SSAP 21(6) also requires change in cash surrender value be reflected on the owner’s statement of income as “Details of Write-ins Aggregated” on line 14 for “Miscellaneous Income.”

Sample journal entries

| Premium Payment

Aggregate Write-ins for Other Than Invested Assets Cash |

Debit

$25,000,000

|

Credit

$25,000,000 |

| Change in surrender value

Aggregate Write-ins for Other Income Gain on Investment in ICOLI |

$1,750,000 |

$1,750,000 |

Tax Reporting

Internal Revenue Code section 6039I and the associated Treasury Regulation section 1.6039I-1 require the owner to attach Form 8925 to its tax return for each year they own the policy. Form 8925 must include the number of individuals employed by the insurance company, the number of employees it insures, the total amount of death benefit covering the insured employees and whether valid consent was obtained from an insured employee. The insurance company must keep a record sufficient to show that proper notice and consent was obtained from the insured employee.

Underwriting

The life insurance company issuing ICOL conducts a simplified assessment of the purchasing insurance company to ensure it is financially capable of purchasing the ICOLI. This financial assessment is conducted using the publicly available statutory filing of the purchasing insurance company and typically requires no additional financial information from the purchaser.

In addition, the life insurance company issuing ICOLI requires a census of proposed insured employees and will determine if the group meets its guaranteed issue (GI) underwriting guidelines. GI allows the issuing ICOLI company to issue policies without requiring any medical underwriting. The proposed insureds must simply answer a few basic questions when providing consent. The questions typically asked are whether the proposed insured is actively at work full-time, whether they have missed work for a recent period due to illness, and whether they are a tobacco user.

Role of the consultant

Pre-purchase and implementation

During an insurance company’s exploration of ICOLI, the consultant provides:

- information on the tax, accounting, financial, regulatory, risk and rating impacts of a purchase,

- financial modeling of various life insurance product structures,

- life insurance company study of available products,

- financial comparison of various ICOLI products,

- draft materials for presentation to the board of directors,

- negotiate life insurance policy contract pricing terms, and

- management of the acquisition and implementation process.

Post-purchase ongoing administration

A consultant provides the following ongoing services:

- servicing the ICOLI for the life of the policies or help the client select a third-party recordkeeper to conduct ongoing administration.

- Administration includes: quarterly investment reviews, assisting in the preparation of annual IRS compliance and state regulatory reporting materials, providing periodic accounting reviews, supplying applicable carrier investment menu updates, conducting annual issuing carrier reviews to ensure ongoing dedication to the marketplace, and more.

- The consultant must also be capable of keeping an up to date understanding of the ongoing tax, legal, investment, accounting, regulatory, and rating environment and how it affects the ICOLI policyowner.

Conclusion

ICOLI is an effective tool for hedging benefit liabilities and improving investment yield. The path through education, design, carrier selection, implementation, and into ongoing administration can be significantly streamlined if the purchaser engages an experienced consultant.

This information is for general and educational purposes and not intended as legal, tax, accounting, securities, or investment advice, nor an opinion regarding the appropriateness of any investment, nor a solicitation of any type. Information obtained from third-party sources are believed to be reliable but not guaranteed. #3851795.2

Disclaimer: The materials are designed to convey accurate and authoritative information concerning the subject matter covered. However, they are provided with the understanding that Mullin Barens Sanford does not engage in the practice of law, or give tax, legal or accounting advice. For advice in these areas please consult your appropriate advisors.

© 2025 Mullin Barens Sanford Financial and Insurance Services, LLC. All Rights Reserved.

1421 Emerson Avenue, Oxnard, California 93033 | Main (650) 740-7773 | Website: www.mbsfin.com

Securities offered through M Holdings Securities, Inc., a Registered Broker/Dealer, Member FINRA/SIPC. #4444620