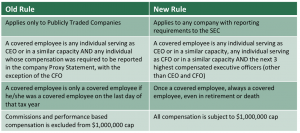

This alert serves as part two of a two-part alert regarding changes to section 162(m) of the IRS tax code. Part two focuses on recommended steps to maintain and maximize grandfathered compensation, particularly in Non-Qualified Deferred Compensation (NQDC) Plans. If you have not read part one of this notice, please visit the Mullin Barens Sanford Financial website here to familiarize yourself with the law changes. The chart below provides a brief comparison of section 162(m) before and after the rule change.

Recently, the IRS issued Notice 2018-68, providing guidance under Section 162(m) of the Internal Revenue Code, as amended by the 2017 Tax Cuts and Jobs Act (the “2017 Act”). Section 162(m) disallows the deduction of compensation paid by public companies to covered employees to the extent such amounts exceed $1 million per year. The 2017 Act changed the definition of covered employees, expanded the entities subject to Section 162(m), and eliminated the exception for commission and performance-based compensation. Application of the new rules commences in 2018, except that compensation paid pursuant to a binding written contract that was in effect on November 2, 2017, is grandfathered as long as such contract is not material modified after that date.

Grandfathering of Compensation

IRS guidance has significantly tightened rules for deducting executive compensation, but it has also provided an avenue for some compensation to be grandfathered to maintain deductibility. The provision is based on the premise of allowing compensation which has already been promised to an executive with a binding contract to be grandfathered. However, if the contract permits either party to modify the level of compensation it will not be grandfathered. Further still, the ability to reduce compensation or cancel the contract will minimize grandfathered compensation. Generally, accrued balances in NQDC plans will be grandfathered, even if compensation will be paid after the November 2, 2017 deadline. However in many cases, the company has authority to unilaterally terminate a NQDC plan or change the investment crediting options which may prevent future interest on existing balances to be grandfathered.

Determining 162(m) Deductibility in an NQDC Plan

In order to determine if plan balances in an NQDC plan are deductible, plan sponsors must assess whether balances would have been deductible under old rules and then bifurcate balances which are deductible from those which are not. This must be done on an employee by employee basis, considering several factors as outlined below.

Covered Employees

Recall that only “covered employees” are subject to the $1M compensation deductibility limit under section 162(m). The account balance of any participant who was not a covered employee before November 2, 2017 can be grandfathered as of that date. Of particular importance is the CFO of the plan sponsor. Prior rules did not consider the CFO a covered employee, but the new rules do. As such, the CFO’s balance as of November 2, 2017 should be grandfathered and so deductible at the time of distribution, but any additional accruals thereafter will be subject to the limit.

Performance Based Compensation

Perhaps the most impactful change to 162(m) is the removal of the performance-based pay exemption. However, even if an employee was a covered employee while contributing to the plan, if the contribution came from performance-based pay, the employee’s account balance as of November 2, 2017 may be deductible at distribution.

Time of Distribution

NQDC plans have historically been an excellent strategy for allowing more compensation to be deductible under 162(m) by deferring applicable compensation into retirement-after an employee is no longer a “covered employee.” However, under the new rules covered employees are still covered after termination. Account balances as of November 2, 2017 which are distributed post termination may still be grandfathered, but future accruals will be subject to the new rules in the year of distribution. However, the total amount payable to a retired employee is likely to be significantly less during retirement such that nonqualified deferrals are still an important way to minimize the application of 162(m).

Ability to Terminate the Plan

If the plan sponsor does not have the unilateral ability to terminate the plan, the NQDC plan document will likely act as a binding written contract 162(m) purposes. This binding contract allows promised compensation to be deducted, including balances contributed before November 2, 2017 and the minimum guaranteed crediting rate outlined in the plan.

Conclusion

Recent IRS guidance has clarified how they interpret and will administer the redefining of Section 162(m). While guidance has severely limited ability to grandfather compensation, NQDC plans allow several avenues for deductibility of current plan balances. In order to take advantage of these avenues, plan sponsors must consult with outside counsel to review the NQDC accounts of their covered employees to maximize deductibility at a future distribution.

Another consequence of this IRS guidance is the newfound prominence of NQDC plans in managing tax consequences of future compensation. While new rules have effectively removed exemptions from the $1M limit, NQDC plans can still allow plan sponsors to spread compensation over several years-minimizing the tax burden in any one year. Consult with your contact at Mullin Barens Sanford Financial to learn more about how an NQDC plan can assist in tax planning surrounding Section 162(m).

About Mullin Barens Sanford Financial

Through a powerful combination of independence and experience, Mullin Barens Sanford Financial and Insurance Services (MBS Financial) is a leading consulting firm that assists companies with 409A and other executive benefit needs.

Disclaimer: The materials are designed to convey accurate and authoritative information concerning the subject matter covered. However, they are provided with the understanding that Mullin Barens Sanford does not engage in the practice of law, or give tax, legal or accounting advice. For advice in these areas please consult your appropriate advisors.

© 2025 Mullin Barens Sanford Financial and Insurance Services, LLC. All Rights Reserved.

2242 Purdue Avenue, Los Angeles, California 90064 |Website: www.mbsfin.com

Securities offered through M Holdings Securities, Inc., a Registered Broker/Dealer, Member FINRA/SIPC. #4444620